The Layman’s Guide to Accounting Part 1

The Layman’s Guide to Accounting Part 1

Basics of Accounting

Introduction to the Layman’s Guide Series

The Layman’s Guide series is a series of short articles going over particular aspects and principles of fields normally considered complicated or too academic for the average person. Emphasizing the principles and ideas that an average person may encounter in their daily life, while tying them together to the discipline as a whole, The Layman’s Guides are intended to be both a reference and an introduction. It is in essence what I wish I had when I was younger, a series of articles explaining key principles of a profession that allow one to begin exploring the field more holistically. I attempt to replicate the comprehensive encyclopedia articles of yore – and where better to start than something I actually went to school to do?

Let’s dive right in.

The Three Categories – Assets, Liabilities, and Equity

Assets, liabilities, and equity. These are probably the three most popular accounting terms that people are aware of, and for good reason – they’re also the most important. For any accounting entity, be they individual, sole proprietorship, partnership, or corporation, these three things are absolutely universal. They are defined as follows:

Asset – Property owned by the accounting entity considered valuable and able to meet debts or obligations.

Asset (short definition) – All your good stuff.

Liabilities – Obligations, particularly debts, owed by the accounting entity. Essentially, everything the accounting entity owes – or, in other words, how much of your stuff other people actually own.

Equity – Assets minus Liabilities. Essentially, how much of what you own do you actually own, or what you would theoretically be left with if you had to sell assets to pay your debts.

Liabilities & Equity (short definition) – Who actually owns all your stuff. Liabilities are owed to others, while Equity is how much you actually own.

These three are very broad categories, and are each subdivided into accounts, representing the different types of assets, liabilities, and equities. These are in turn edited by entries, kept in ledgers that record individual transactions. These are our next subject – the actual meat and bones of accounting.

The Three Tools – Accounts, Ledgers, and Entries

Accounting’s most important function is to keep track of the flow of money and value. This, however, comes at a cost – in that recording transactions takes time and effort away from actually making the transactions. Hurrying the process costs the expense of making, tracking down, and unwinding mistakes, while taking the time to meticulously record every transaction costs revenues in lost time. As such, the process of accounting is designed to balance brevity and accountability, attempting to achieve quick recording of transactions in the moment and the ability to trace back any mistakes.

The System of Accounts

Accountants’ accounts have a simple goal. Everything must fall into one of the three categories of assets, liabilities, and equity, based on their use to the accounting entity. These accounts are the general categories of things most often used by the accounting entity. Examples are assets such as cash to represent actual bills and coins, bank deposits, and other riskless financial products, receivables for debts owed to the entity, inventory for businesses with merchandise or work in progress, and so on. Liabilities will typically be split into current liabilities (falling due within a year) and non-current liabilities (falling due beyond a year). Current liabilities include accounts payable (current debts owed to the entity). Non-current liabilities are often put down as loans payable (non-current debts owed to the entity). Owner’s equity depends on the ownership structure – owner’s equity for a sole proprietorship, individual accounts per partner for a partnership, and shareholder’s equity for a corporation.

The astute may have realized that I have not yet mentioned revenues and expenses. Revenues and expenses belong to what is called temporary accounts – accounts meant to record transactions for a period before being “closed” to permanent accounts at the end of a financial reporting period (usually a year). While you could make the entries directly to the permanent accounts, establishing temporary accounts for revenues and expenses of different types allows for more accurate record-keeping and clearly delineating different sources of changes to the permanent accounts. It would be correct but careless, for example, to lump all your expenses as credits to cash and debits to owner’s equity, without being able to tease out which are legal expenses, lease expenses, and the owner slipping receipts into the till to make the company pay for them[1].

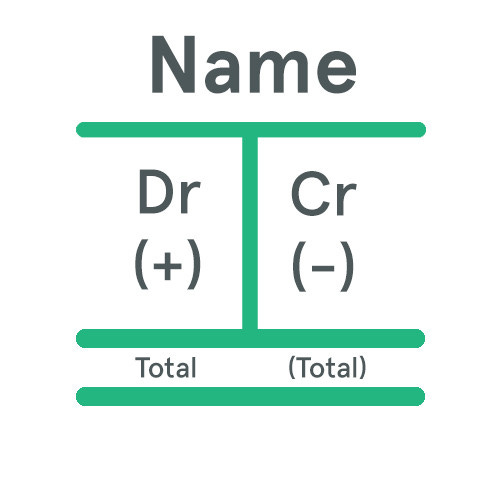

The most basic representation of these accounts is via T accounts, as seen below.

Accounts are divided into two halves, the left side traditionally for debits, the right traditionally for credits. We’ll explain this later on, but for now, just take it on faith that one side adds to the balance, while the other subtracts, and that each account will normally end the period with a positive total on one side or the other. If everything goes right, it will all balance in the end.

The Ledgers and Records

A ledger is where daily entries are recorded before being posted to the relevant accounts. Most important to us is the general ledger – simply put, a ledger where all the entries are recorded before being totaled at the end of the day and posted to their accounts. While the accounts focus on traceability, the ledger entries focus on completeness. Meant to accompany staff or bookkeepers in the field before being submitted to a head office and put in the accounting system, the ledger is, by itself, an important tool to collect all the relevant entries of the day.

You’ll notice immediately that the ledger notebook has six pairs of two columns, just like the T account. These are there for the same reason - to record debits and credits. The particularly wide column preceding the pairs of columns is for account names, as ledgers are meant to collate all entries before they are posted to the accounts proper. Rather than organizing by type of asset, liability, or equity, as the general accounts do, the ledger accepts all transactions to be sorted out later. This particular ledger is likely a summary ledger, totaling up receipts or other ledgers where entries were first recorded before being posted to this ledger.

Of courses, that raises the question of how these entries are made, as we will soon see.

The Entries

Accounting entries follow a strict rule of double-entry bookkeeping. Double-entry bookkeeping is the principle that for every debit, there is a corresponding credit. Debits represent entries that add to assets or reduce liabilities or equity, while credits are the opposite, reducing assets or adding to liabilities in equity. When recorded on a ledger, debits are recorded on a left-hand column, while credits are recorded on the right, meaning that in theory, every ledger should “balance”, with an equal amount of debits and credits[2]. Conveniently, this also means that when the ledgers post entries to the system of accounts, all the debits and credits across all the accounts should add up to an equal amount, and therefore balance. This simultaneously allows for a convenient way to check if the procedure was performed correctly (if it was not, the debits and credits would not equal, known as balancing the books), and recognizes that the accounting entity owes everything to someone else, be it the creditor or the owner.

A quick example will likely be instructive. Say you start a corporation separate from yourself with 10,000 US Dollars in shares. This counts as a purchase of your own shares, like so:

Debit (dr.) Cash (an asset account) $10,000/Credit (cr.) Owner’s Equity (an equity account) $10,000.Then, you take out a loan in the name of the corporation for $5,000, like so:

Dr. Cash $5,000/cr. Loans Payable (a liability account) $5,000You then proceed to purchase some merchandise with cash,

Dr. Merchandise Inventory (an asset) $5,000/cr. Cash $5,000Pay for a ticket and a convention booth, or a bazaar stall, or so on

Dr. Location Expenses (an expense account) $500/cr. Cash $500and now you only have to wait for the day of sale. On the day of the convention, you sell out $2,000 worth of inventory for $2,500, resulting in the following entries.

Dr. Cash $2,500/cr. Sales Revenue (a revenue account) $2,500Dr. Cost of Goods Sold (an expense) $2,000/cr. Merchandise Inventory $2,000When all is said and done, you close your temporary accounts to the corresponding permanent account. Sales revenue, Cost of Goods Sold, and Location Expenses are all temporary accounts. Revenues and expenses (other than interest expenses and debt repayments) are usually closed directly to equity, in this case, shareholder’s equity. Since sales revenue has a credit balance, it should be debited and the same amount credited to equity. Cost of goods sold and location expenses have a debit balance, so they need to be credited to zero and then owner’s equity debited for the balance. Following this procedure, we make the following entries:

Dr. Sales Revenue $2,500/Cr. Shareholder’s Equity $2,500Dr. Shareholder’s Equity $2,000/Cr. Cost of Goods Sold $2,000Dr. Shareholder’s Equity $500/Cr. Location Expenses $500As you credited and debited equity for an equivalent amount, it is easy to see that you have at least broken even on this venture so far – not the best first foray into business, but not the worst, either.

If we add up the sum total of all the debits and all the credits we made, the amount comes to $27,500 of debits and credits, neatly balancing the books on both sides.

Accrual vs. Cash Basis

In the real world, many purchases are made on debt – or as you now understand, on credit. Talking about this will bring us to one of the most important rules of accounting, the assumption of accrual accounting winning out over cash accounting. To start, let us imagine that after your showing at the convention, you make some sales online in the amount of $500 based on $400 of merchandise inventory and $20 of shipping. The question now emerges – you have agreed to sell the goods, but the customer has not paid cash to pay for them. All you have is their debt – say, via credit card, or a written contract. Still, if they flake on you, you’re at a loss for sure.

This is one of the judgments that underpin accounting, and while it might strike you as a small matter, accounting is used to value and understand the transactions of all companies, from the largest to the smallest. Without a consistent principle, accounting loses its ability to communicate the financial position of all different companies, and therefore the profession must make a clear choice on how to communicate the underlying phenomenon.

In this case, accountants have come down on the side of accrual accounting. Accrual accounting recognizes sales and expenses “as earned”, or when the good or service is provided or agreed upon, rather than when the cash is paid. The cash basis, by contrast, would only recognize the sale upon payment of cash. The accrual series of entries is shown below:

Dr. Accounts Receivable (an asset, this is owed to you) $500/Cr. Sales Revenue $500Dr. Cost of Goods Sold $400/Cr. Merchandise Inventory $400Dr. Shipping Expenses – Inventory $20/Cr. Cash $20For cash, however, you would not be able to credit sales revenue, as you could not recognize the sale. It would be premature to credit owner’s equity directly, so we credit an account specifically made for this situation – Deferred Revenues. The other two entries remain the same.

Dr. Accounts Receivable (an asset, this is owed to you) $500/Cr. Deferred Revenues $500Dr. Cost of Goods Sold $400/Cr. Merchandise Inventory $400Dr. Shipping Expenses – Inventory $20/Cr. Cash $20When the cash is received, however, the entries will also be different. The accrual basis entry is shown below:

Dr. Cash $500/Cr. Accounts Receivable $500For cash entries, a little more finesse is required:

Dr. Deferred Revenues $500/Cr. Sales Revenues $500Dr. Cash $500/Cr. Accounts Receivable $500We can see here that cash lost out at least partly due to duplication of effort. Another key reason is that many business-to-business transactions are done on credit or consignment, all of which would make for a very large number of deferred revenues on company income statements. This, however, also has a disadvantage – it can make companies that are insolvent and unable to service debts still look very attractive. Imagine a company that accepts an order for merchandise with sale value of $100,000 payable in three months. The customer is in turn unable to sell the merchandise and goes bankrupt, completely unable to pay their debt. The entries are shown below:

Dr. Accounts Receivable $100,000/Cr. Sales Revenue $100,000Then, when the bankruptcy is discovered:

Dr. Bad Debts Expense $100,000/Cr. Accounts Receivable $100,000 (as the company is bankrupt with no remaining assets, this account can no longer be received).And when the revenues and expenses are closed to income:

Dr. Owner’s Equity $100,000/Cr. Bad Debts Expense $100,000.For the period between the recognition of the sale and the discovery of the bankruptcy, the company appeared to be selling well, even if it was making sales that it could not collect on in cash. This makes the company appear more profitable than it is, only to recognize an expense when the bankruptcy occurred. This, in turn, was only possible because the sale was recognized before cash changed hands.

Conclusion

Accounting is a system of accounts, ledgers, and entries meant to make it easy to record, represent, and communicate the financial position and flows of an accounting entity. In order to be as universally useful as possible, it follows a set of guidelines embodied in the International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP), both of which govern how accounting interprets events. This, however, necessarily creates loopholes such as the one shown by accrual vs. cash basis accounting, thanks to the assumptions made to simplify interpretation of the process, as in the mechanism I described previously in Communication Overhead, with IFRS and GAAP serving as Organizing Principles.

Another key idea is the general rule of double-entry bookkeeping - that every change is attributable to another account. While as long as we stay in the realm of the commonplace, this is quite reasonable, things quickly become difficult when we come face-to-face with the volatility of the market. Particularly when dealing with share transactions, financial assets, and other ideas, the world of accounting is full of thorny issues, particularly since appraisal and valuation of goods falls outside the purview of accounting.

In the next installment, we’ll move on to interpretation and tackle the three financial statements – the statement of financial position (balance sheet), the income statement, and the statement of cash flows.

[1] I think that last one is called embezzlement, though since it’s the owner, it’s probably more a case of fraud.

[2] By the way, this is how debit and credit cards got their name. Debit cards reduce the balance of your savings account, and therefore, the bank’s cash liability to you, which the bank records as a debit. Credit cards increase your debt or liability to the bank, which you record as a credit.