The Layman’s Guide to Accounting, Part 3

The Layman’s Guide to Accounting, Part 3

Due Diligence Voodoo Doodoo

The Layman’s Guide series is a series of short articles going over particular aspects and principles of fields normally considered complicated or too academic for the average person. Emphasizing the principles and ideas that an average person may encounter in their daily life, while tying them together to the discipline as a whole, The Layman’s Guides are intended to be both a reference and an introduction. It is in essence what I wish I had when I was younger, a series of articles explaining key principles of a profession that allow one to begin exploring the field more holistically. In this third part of The Layman’s Guide into Accounting, we look at how to do your due diligence and look into companies you’re interested in. If you missed the first part, it’s here, with the second part here – both of which you’ll need.

I assume here that you already know what company you’re interested in, be it your own or an investment prospect. To help you follow along, I’ve decided to use that’s both new to me and in an industry new to me – Oracle Cerner – suggested by

.Finding your Filings

The most important component of analyzing a company’s financials is, naturally, finding them. Filings are commonly done yearly and quarterly, mandated by your country’s Securities and Exchange Commission (SEC) or equivalent. All of these filings contain a report on the company’s financial status and activities during the period, along with a comparison to the previous period (last year for annuals, or the same quarter last year for quarterlies). Privately-held companies can choose who to give these information to, but publicly-listed ones must provide this information to the exchange they are listed on every year.

For the individual, though, it’s pretty simple. Go to the company’s website and scroll to the bottom to look for the magic words.

Following “Investor Relations” leads to this page, for Oracle as a whole where you’ll get a lot of information. The most important thing we learn is that Oracle Cerner files under Oracle Corp., which will be important later. For our purposes, the important ones are “Financials” and “SEC Filings” – look for either or both. Oracle, listed on the New York Stock Exchange and incorporated in the United States (Delaware, to be precise), must file annual and quarterly reports called Forms 10-K and 10-Q, respectively. These contain audited financial statements and legally required disclosures to the SEC, making them the most reliable source of information on a company that you can find, and one that most companies will have publicly available.

For this exercise, I’ll be covering only the annual 10-K’s for Financial Year 2023 and 2022 (under the Q4 hyperlink for the 10-K and 10-Q row).[1]

Finding Cerner

Since we’re dealing with Oracle’s financial statements, rather than those for Oracle Cerner in particular, the first and most important question to ask is… can we find them? Because Oracle owns Cerner, isolating Cerner itself as a business concern may be impossible, since it becomes a part of the wider company, and wouldn’t necessarily be reported separately.

In order to do that, we first have to find out how, and how much, Oracle owns Cerner. According to the 2022 10-K, Cerner Corporation, a provider of digital information systems and health systems that support medical professionals, was acquired for approximately 28.2 billion US Dollars (USD), borrowing 15.7 billion USD of that amount[2], on June 8, 2022. This made Cerner an indirect, but wholly-owned subsidiary of Oracle[3], being merged into Cedar Acquisition Corporation, a wholly-owned subsidiary of Oracle Corporation, as per Oracle’s 8-K filing, helpfully linked on page 112 of their 2022 10-K. The 8-K filing is an Agreement and Plan of Merger, filed to notify the SEC of the intention and agreement of the parties to engage in a merger.

All that to say that these financial statements are completely consolidated under Oracle, and we can no longer tease out the particular figures for what used to be the Cerner Corporation, now Oracle Cerner. As a wholly-owned subsidiary, there’s no reason to report Cerner’s results separately, unless it is required – for example, if Cerner Corporation was publicly listed, and remained listed, it would still have to file disclosures. This not being the case, we can no longer isolate Cerner’s financial performance. That being said, we’ve got some perfectly good 10-K’s right here, I might as well use them anyway.

Querying the Oracle

This being a layman’s guide to accounting, we focus on the audited financial statements and their notes, starting on page 64 of the 10-K filing and continuing until the end. The preceding parts talk about business operations and legal proceedings, business and market risks, and matters for the stockholders and board of directors. There’s important information in there about business strategy and potential risks, but to prevent this piece from taking, and being, even longer than it already is, we will refrain and focus on the financial statements.

The most important first step in deciding how to look at a company is, naturally, why you want to look at the company in the first place. Someone who works there or transacts with the company may be more interested in business continuity – making sure that the company can continue to operate. An aggressive investor looking for capital appreciation will be interested in growth prospects and whether the firm has growth prospects on the horizon, or is in a space that is projected to grow. A more defensive investor might be more interested in the dividend yield rather than wild swings in the stock price, focusing on how much is paid as dividend compared to the market rate, and whether the company has the ability to service said dividends. Bigger companies may be looking into acquiring the listed company, meaning that they have an eye more on their technologies, capabilities, and market position just as much as their financial performance. These four preferences will be summarized below:

Transactors represent the people who want to check up on their employer, supplier, or client. Their focus will be on the company’s continued viability, rather than their growth. We assume they are likely not interested in investing in the company’s equity, as transacting with the company regularly already gives them an implicit stake in the company, as I’ve written before in the Life Portfolio concept.

Defensive Investors represent investors that are interested in buying the company’s shares for their dividend yield and holding it for a long period of time, taking any capital appreciation as a bonus to their strategy. Often associated with older investors and pension funds, defensive investing is usually done in mature sectors with relatively low valuations (and higher dividend yields).

Aggressive Investors represent investors that are interested in buying the company’s shares for the capital appreciation and holding it only as long as they need to reap a profit. This is where your longer-term investors sit – technical traders focus more on the stock price than anything else. These are the guys you probably think of when you hear “speculators”.

Acquirers represent other companies or funds that are interested in buying a lot of the company’s shares as a business move, whether it’s to own the company entirely and bring in their capabilities, as Oracle did with Cerner, to get a foothold into a new market, or any other business-minded motivation.

Once you’ve decided on why you want to look at this company, we can move on to a quick overview of what I fond in the company’s financials.

The Basics

Oracle Incorporated, as of the end of financial year 2022, approximately 21,383,000,000 US Dollars in cash and cash equivalents. Taken in isolation, however, that information actually tells you very little. Is it enough for them to service debt? Unless you know how much debt they have, you don’t know that. How long will the company last without access to new sources of cash? You wouldn’t know unless you had access to how much they routinely spend. For the purposes of financial analysis, there are many times where the absolute number doesn’t matter as much as the relationship, or ratio, between two particular numbers. This is where we do what’s called vertical analysis – the comparison of the company’s accounts in relation to each other in order to shed light on the company’s performance.

The most fundamental way of doing this is through the common-size balance sheet and income statements, which involve converting the different accounts on both statements to percentage values. This takes advantage of the balance sheet’s Total Assets and Total Liabilities and Equity accounts being the largest in their respective section and equal to one another, allowing them to form the base for the 100%. Total Revenue on the income statement works in the same way, forming a 100% base against which all other quantities can be measured.

A quick and dirty Excel version of Oracle’s FY 2021-2023 gives a balance sheet as below:

Looked at like this, we can see clearly what the most financially important parts of the company are. The balance sheet is clearly dominated by net goodwill, and long-term notes and liabilities. The former, net goodwill, represents the estimated value of a company’s intangible assets – brand name, reputation, software, and so on – that is recognized on the balance sheet. This is most often measured by what is called “economic goodwill” or, simply, paying more for a company than it’s worth – that worth being measured by net assets, or total assets minus total debt[4]. More can be read about it here for those reporting in GAAP and here for those reporting in IFRS (likely you if you’re not in the US). Going from one-third to one-half of Oracle’s total assets, goodwill is a very important part of the company, and, as we’ll see later, one that needs to be taken into great consideration when evaluating the business.

On the liabilities and equity side, the major item of note is the long-term liabilities and notes payable – representing debt that is to be paid by the company more than a year from now. Clocking in at over half of the company’s total liabilities and equity and rising to nearly two-thirds, these long-term liabilities show who really owns Oracle – its creditors. The balance, however, doesn’t tell us as much as the accompanying notes detailing the amount and rates of said debts (pg. 89 of the FY 2022 filing and 88 of the FY 2023 filing). This also presents a threat to continued operations – namely, that Oracle may have to refinance these loans in a heightened interest-rate environment, or suffer by having to sell off businesses or products in order to pay off debt and continue operations. When we get into financial ratios later, we’ll dig into how to work this out. For now, though, let’s move on to the income statement, and see how Oracle makes its money.

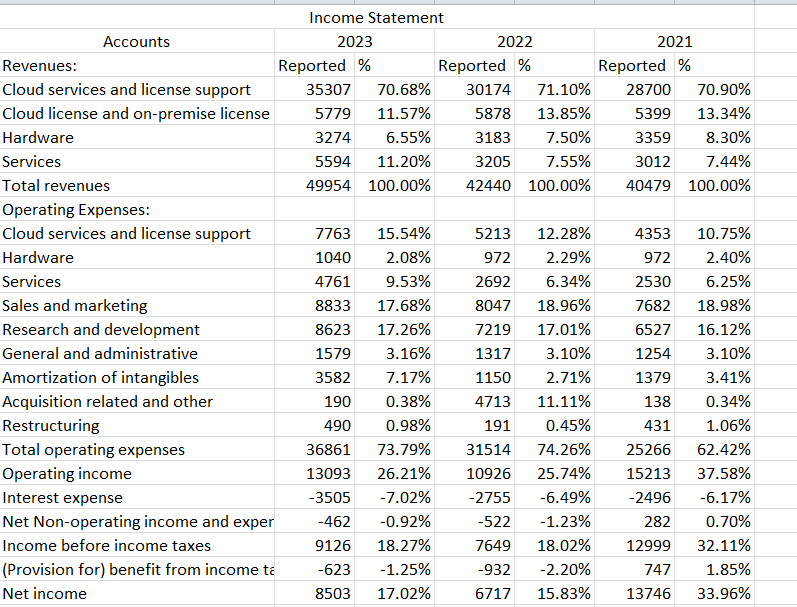

We can see that almost three-fourths of Oracle’s revenue comes from an item called Cloud Licenses and Service Support. Checking the relevant note (Segment Information, pg. 104 of the FY 2022 filing and pg. 103 of the FY 2023 filing) reveals that this item refers to sale, marketing, and delivery of enterprise products. In other words: selling software to big businesses that need to outsource their data management. This dovetails nicely with the roughly three-fourths of revenue spent on operating expenses, leading to a roughly 25% operating margin bitten into by a small, but growing to 7% interest expense leading to pre-tax income of roughly 18% in FY 2023. We can see in the statement that these numbers were markedly better in FY 2021 (June 1, 2020 to May 31, 2021), likely owing to the lower costs of everything (note that operating margins decreased drastically between FY 2021 and FY 2022, likely coinciding with high inflation in the hot markets of 2021 and 2022). This presents a danger, though probably not a current one, to Oracle – high inflation and rising interest pushing the company out of profitability could happen, but its position in a market central to the modern Information Age economy generally precludes such a notion[5].

The bottom of the income statement also presents us with our first ratio, earnings per share. This is simply net income divided by the number of common shares outstanding – essentially, how much participation each share has in the earnings. This is an important component in how companies are valued, most popularly in the famous P/E or Price to Earnings ratio, which puts the share price over the earnings per share to determine if a stock is over- or undervalued. Ratios help put things into perspective and normalize across companies of different sizes, which is very important when comparing different investment prospects.

The decrease in weighted average shares outstanding below owes to stock buybacks – an alternative to dividends when it comes to returning money to the shareholders, usually undertaken by a company as a mark of confidence in its own future prospects. Stock buybacks are also great for pushing up the price of a stock, thanks to rising earnings per share and the company sending the signal that the future is bright. Unlike dividends, it also doesn’t signal a commitment to long-term payouts, making it a less committal alternative. This also neatly reminds us that the companies know ratios too, and are happy to game them in order to juice the share price.

My Overall Assessment

In my estimation, Oracle is in a good place, though economic headwinds may dampen its current prospects, the company has a lot of room before anyone should be worried.

This is based on the (still) large net income margin of 17% and the operating margin of 25%, backed up by high operating cash flows (reaching $17 billion in FY 2023), showing that Oracle’s core business – the provision of technology licenses and software to enterprise customers – works to generate profitable cash flows and are therefore not likely to be divested. Revenue has grown year on year every year, and although times could be better, they could certainly be worse. Costs keep in line with revenues and the corporation continues to grow.

However, there are threats on the horizon that are already beginning to bear their fangs. The bite of costs is noticeable in Oracle’s filings – a quick look at the income statement for 2021 and comparing it to the two years hence shows a drop in profitability despite growing revenues. At the same time, interest expense as a percentage of revenues has crept up to 7%, thanks to interest rates worldwide staying high to stem inflation, debts must be renewed at the current higher rates. Continued acquisitions of companies such as Cerner has increased the balance of goodwill (an intangible, illiquid asset of no help in a bankruptcy), along with the long-term debt load to finance said purchases. This could leave the company strapped for cash, a fact borne out by cash only being 7% of total assets in FY 2023 (from around 20% in years prior). All these factors combined point to two things – cost-cutting and revenue-hunting to shore up the company’s cash position, which could spell trouble for business partners who are feeling the bite. If economic headwinds persist, Oracle could have some trouble on their hands.

The most important information, however, is often found off of the filings, and this is it – Oracle Corp is one of the leading companies and innovators in the space, with the largest asset base, and likely one of the widest and most diversified network of enterprise clients. In short, a lot has to go wrong for a lot more people before Oracle is truly affected. The high share price, still hanging at around $112 per share, shows general confidence in the company’s continued performance. I wouldn’t be worried for this company any time soon.

The Limits of Accounting

I want to take some time now that we’ve gone through a simplified version of the process of financial analysis to point out some of the limits of this process. These are the important things that the big-money firms worry about that the itinerant investor might not even know are problems, which can skew your analysis and change your world.

Choose Comparables Wisely

I talked a lot about ratios and common-sized balance sheets as methods of allowing us to compare companies in order to evaluate relative performance, but in this essay, I never did that. This is for two reasons; first, I don’t know Oracle’s core business and competitors well enough to pick suitable comparables, because I’m not sure what companies out there are in a similar line of business or would have remotely comparable financials. This is very important, since comparable companies need to have a similar enough business model to be benchmarks – it wouldn’t do to compare Oracle to something in the agricultural sector or a quick-service restaurant. The second reason is the large number of acquisitions Oracle has made. It can become difficult to disaggregate the many different companies’ contributions to revenues and find a company that works in a similar way, with lots of fingers in lots of pies. This leads smoothly into the next point below.

Goodwill is Fickle

I brought up pretty early on that Oracle’s balance sheet is dominated by two accounts – goodwill taking up almost half of total assets, and Notes Payable taking up almost two-thirds of total liabilities and equity. These two accounts tell you that Oracle has either invented or acquired a lot of companies, as goodwill is an account showing the estimated value of intangible assets such as brand names, proprietary technology, and other such assets. Most commonly, however, goodwill is recognized when a company acquires another company for more than the authorized paid-in capital of the target company – in other words, through acquisition. Let’s have a fictional, incredibly oversimplified example.

Dungeons Limited, a corporation in good standing, wants to acquire Dragons Corp, also a corporation in good standing. The latter has an authorized paid-in capital of $1,000,000, while the former has agreed to pay $1,100,000 for the company. The surviving entity, Dungeons & Dragons Inc., has a problem.

The two sides of the balance sheet should always balance – that’s the whole point. Let us imagine the entries that we could make for this transaction. Obviously, since we are paying cash to the shareholders of Dragons Corp, we are paying cash in exchange for their authorized paid in capital – their stake in the company. Let’s make our entries:

Dr. Dragons Corp Purchase Expense $1,000,000/Cr. Cash $1,100,000This doesn’t balance, because we can’t buy more than the amount of capital booked, but we also paid more than that. We need somewhere to debit the additional $100,000 to in order to balance the books – and that’s where goodwill comes in, like so:

Dr. Dragons Corp Purchase Expense $1,000,000, Dr. Goodwill $100,000/Cr. Cash $1,100,000This is how goodwill is born – as a balancing figure to explain why you overpaid for a company. As such, being subject to all the difficulties of estimation and the dangers of paying a lot for something that isn’t there, it should be treated with some caution. Usually, such takeovers are debt-financed, which leads smoothly into the next point.

Oracle has a large but not unmanageable debt load as evidenced by its Notes Payable balance, that it uses to pay for its acquisitions of other companies that allows it to maintain its market position and leverage existing expertise in new areas. This implies, however, that constantly increasing debt and goodwill is an important part of the business model, meaning Oracle will need to issue new debt and roll over existing debt. This creates a danger of overreach – borrowing too much to buy more companies will cause growing interest expense and illiquidity that could threaten the company’s operations, believing that this will be justified by maintaining its market position. While I agree, and believe that management has handled this risk well so far with long-term fixed-rate debt, continuing recklessly with the strategy could cause great difficulties in cash flow, leading to cost-cutting or revenue-pumping in the coming years.

Conclusion

This is the third part of the Layman’s Guide to Accounting, and wow, is it long. More intricate methods of valuation and anlysis, like industry comparisons or discounted cash flows, would have blown out the length of this piece and made it hard to digest, but if there’s interest, I can cover those as well. Leave any follow-up questions or requests for me to cover more things in the comments, along with how you see Oracle Corp and its future. Also leave your suggestions to what I should cover for the next part, or if I should start a new guide in your wheelhouse, so you can see me struggle with what you know how to do.

[1] Anyone following along may notice that Oracle somehow already has entries for Financial Year 2024 Q1, despite it not being calendar year 2023. For some seasonal businesses,

[2] Pg. 57, Oracle 2022 10-K, Credit Agreements and Related Borrowings

[3] Pg. 85, Oracle 2022 10-K, Note 2 to the Audited Financial statements.

[4] As I’ve said in the previous part, all the assets in a company are owed to somebody – and if it’s not the creditor, it’s the owner.

[5] I base this on Oracle’s revenue growth. Despite everything, revenues have grown substantially, showing Oracle has either pricing power or the ability to grow sales to meet this threat.

This is amazing! Thanks for writing this Argo, and for taking the example of Oracle. Really great stuff.